Last Wednesday's Fed report hit different than usual. When Reuters covered the Fed's monetary policy statement about inflation "stepping up" from tariffs and supply chain pressures, hardware store owners started calling their suppliers immediately. And for good reason.

Elevated rates staying higher for longer plus renewed inflation means your carrying costs just went up while your purchasing power went down. That's a nasty squeeze for businesses already operating on 2-3% net margins.

After spending the morning reviewing inventory data from several hardware stores, the ones who moved fast on specific operational changes are already seeing their cashflow stabilize. The ones treating this like just another news cycle are scrambling to cover increased floor plan costs and supplier price hikes that hit faster than expected.

The triple hit nobody's talking about

Most hardware stores focus on the obvious problem — prices going up. But after helping dozens of stores navigate the 2022-2023 inflation surge, there are actually three distinct operational problems hitting simultaneously that compound each other.

First, your floor plan financing rates jumped. If you're carrying $400,000 in inventory (pretty typical for a 4,000 sq ft store), every percentage point increase costs you another $333 per month. Rates moving from 7% to 9.5% means you're bleeding an extra $830 monthly just to hold the same stock.

Second, supplier payment terms are tightening. Vendors who gave you net-60 during slower periods are pulling back to net-30 or requiring deposits on larger orders. One paint supplier recently changed their terms for orders over $5,000, requiring 25% down. That's cashflow you need elsewhere.

Third, the products moving fastest are changing. Contractors are rushing to complete projects before material costs rise further, so pro-grade supplies fly off shelves while DIY items sit longer. Your standard par levels become worthless when velocity patterns shift this dramatically.

Move 1: Split your inventory into inflation response buckets

Stop managing all SKUs the same way. Break everything into three buckets based on how inflation actually impacts them.

Stop losing sales due to inventory gaps.

Hardzly helps you manage stock levels, orders, and supplier interactions efficiently.

- Unified inventory and sales tracking

- Supplier and purchase order management

- Automated workflow and task scheduling

No credit card required

Bucket A - Fast movers with stable margins (protect these) These are your bread and butter items where you maintain pricing power — contractor-grade fasteners, common lumber sizes, basic electrical supplies. For these, you actually want to increase orders slightly before the next price jump. Set reorder points 15% higher than normal but reduce order quantities by 20%. This keeps product flowing without overcommitting capital. A store in Minnesota saved around $4,200 last month just by adjusting their lumber reorder triggers before the latest price increase hit.

Bucket B - Slow movers with volatile costs (reduce aggressively) Specialty items, seasonal products sitting past their prime selling window, anything turning less than twice a year. Cut these orders by 40-60% immediately. Yes, you'll have stockouts on some things. But carrying a $300 specialty plumbing fixture for 8 months when rates are this high costs more than the lost sale.

Bucket C - High-margin discretionary items (test pricing) Power tools, outdoor furniture, grills. These have enough margin to absorb small price increases without killing demand. Test 3-5% increases on your top 20 items in this category and watch the response for two weeks before going further.

Move 2: Implement Thursday afternoon pricing reviews

Pricing decisions can't wait for monthly meetings anymore. Every Thursday at 3 PM, pull your top 50 SKUs by revenue and check three things:

-

Current supplier cost vs what you paid on the last order

-

Competitor pricing (check online, not just local)

-

Week-over-week velocity change

Keep a simple change log with date and percent change so you can track small adjustments and revert quickly if needed.

If cost increased more than 2% and velocity is stable, adjust pricing immediately. If velocity dropped more than 15%, hold pricing but reduce the next order by 30%.

One store owner showed me their Thursday pricing log — in six weeks, they made 47 small adjustments (most under 3%) that preserved roughly $11,000 in margin they would have lost with their old quarterly review process.

The key is small, frequent adjustments rather than shocking customers with large jumps. Customers barely notice a hex bolt going from $0.49 to $0.51. They definitely notice when it jumps to $0.59 all at once.

Move 3: Restructure vendor relationships based on payment flexibility

Not all suppliers deserve the same treatment right now. Rank your top 10 vendors using this formula:

(Annual purchases × Gross margin %) ÷ Payment terms in days

The higher the score, the more valuable that relationship is in this environment. These are the vendors where you maintain or increase orders.

-

Extended terms (net-45 instead of net-30)

-

Volume rebates on prepaid orders

-

Consignment arrangements for slow-moving categories

-

Split shipments to spread out payment timing

A hardware store in Ohio renegotiated with their fastener supplier and landed net-45 terms plus 2% off on orders over $10,000. That freed up around $8,000 in working capital per month.

Don't be shy about these conversations. Vendors need stable retailers who can weather inflation. If you've been a good customer, they'll usually work with you.

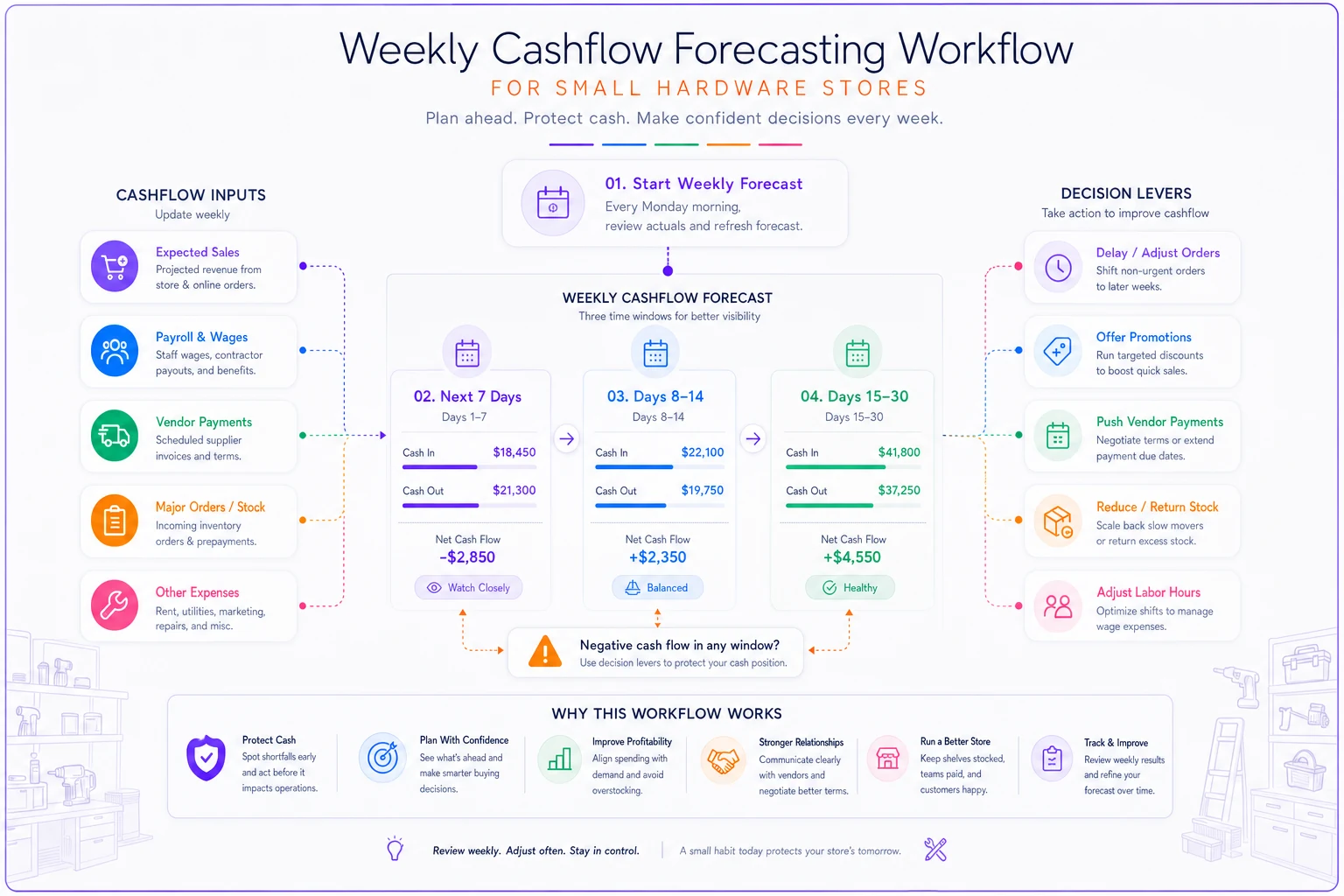

Move 4: Create a weekly cashflow forecast that actually works

Forget complex spreadsheets. You need something you'll actually use every week. Here's the format working for stores right now:

| Window | Items |

|---|---|

| Next 7 days | - Expected sales (last week × 1.05 for inflation adjustment) - Payroll due - Vendor payments due - Loan/lease payments |

| Days 8-14 | - Expected sales - Major orders arriving (requiring payment) - Any unusual expenses |

| Days 15-30 | - Expected sales - Remaining fixed costs |

If cash gets tight in any window, you have specific levers: delay non-critical orders, offer 2% off for immediate payment on receivables, push vendor payments to maximum terms, run flash sales on Bucket B inventory.

This connects directly to the seasonal forecasting routines we've covered before, but with faster cycle times to handle inflation volatility.

Move 5: Rethink your credit offerings

When rates are high, customer financing becomes a competitive advantage — if you structure it right. The old "90 days same as cash" model will hurt you in this environment.

For purchases under $500: No credit, but offer 5% off for cash or debit. Customers feel like they're getting a deal and your cashflow improves.

For purchases $500-$2,000: Partner with a third-party financing company that pays you immediately. You'll pay 3-4% in fees, but you get paid now instead of carrying receivables for weeks.

For purchases over $2,000: Require 25% down, then offer net-30 terms with a 2% early payment discount.

A store in Texas switched to this model and cut their receivables by around $67,000 in two months while only losing three contractor accounts. The cashflow improvement more than offset it.

Move 6: Automate the painful stuff so you can focus on what matters

During inflation, every hour spent on routine tasks is an hour not spent on margin protection. The stores weathering this best have set up automation around:

-

Price change alerts from suppliers (no more surprise cost increases)

-

Reorder point adjustments based on velocity changes

-

Cashflow projections that update daily

-

Inventory aging reports that flag problem SKUs

-

Margin erosion warnings by category

A properly configured operations platform handles these calculations continuously and flags issues before they become actual problems. The owner of a two-store operation mentioned their automated margin alerts caught around $3,400 in pricing errors last month — the kind of thing that disappears into the daily chaos without a system watching for it.

The AI-assisted platforms are genuinely useful here because they can catch patterns humans miss, like when three unrelated SKUs all slow down simultaneously, which often signals a broader category shift worth paying attention to.

What happens if you wait

A hardware store in Florida ran the numbers on their three-week delay in implementing inflation responses. The damage:

-

$4,100 in unnecessary carrying costs

-

$7,300 in margin erosion from delayed price adjustments

-

$2,800 in excess inventory that should have been cut

-

$11,000 in credit line usage that could have been avoided

Total cost of waiting three weeks: just over $25,000. That's two months of profit, gone.

The Fed's report on persistent inflation isn't just economic news for small hardware stores — it's an operational signal that things aren't settling down anytime soon. But stores taking rapid, specific action on inventory management, pricing discipline, and cashflow are proving you can protect margins even in this environment.

Start with Move 1 tomorrow morning. Split your inventory into those three buckets and adjust your ordering immediately. Then get the Thursday pricing reviews going. Those two changes alone will stabilize your operation while you work through the rest.

Your customers depend on you for fair prices, reliable inventory, and the expertise that only a local hardware store provides. These six moves aren't just about protecting your business — they're about making sure your community still has a real hardware store when this inflation wave finally breaks.

Move fast on these, or watch your margins erode while waiting for conditions to improve on their own. Based on what happened to stores that waited during previous inflation spikes, patience isn't the play here.

Ready to elevate your hardware store management?

Join 500+ hardware stores using Hardzly to boost operational efficiency, reduce stockouts, and grow revenue.